TL;DR Africa is not uniformly risky, it is unevenly investable. What markets often price as danger is frequently just noise. The real determinant of returns is not how often countries are tested, but how well their institutions absorb stress when it arrives. By separating agitation from institutional strength, the Investability framework shows why some of Africa’s noisiest markets are among its most investable, while some of its calmest hide the greatest tail risks. For investors, the implication is clear: stop allocating to Africa by headlines and start allocating by institutional resilience.

“A little bit of agitation gives resources to souls and what makes the species prosper isn’t peace, but freedom.” — Jean-Jacques Rousseau, The Social Contract (1762)

Over the past 12–18 months, Africa’s investment story has again been written by headlines: contested elections, coups, currency devaluations, and sovereign debt restructurings1. From FX adjustments in Nigeria and Egypt, to political transitions across West and Southern Africa, to the long shadow of debt workouts in Ghana and Zambia, the message reaching global markets has been familiar: instability equals risk.

For many allocators, this seems to confirm a simple conclusion that Africa is, once again, “high risk.”

But that conclusion rests on a basic mistake. It treats visible stress as a proxy for danger to capital. It collapses political contestation, macro adjustment, and institutional weakness into a single narrative of risk—and in doing so, misses the only question that really matters to investors:

not how often systems are tested, but how they respond when pressure arrives.

That distinction between noise and resilience is where Africa continues to be most mispriced.

What investors routinely misunderstand is not Africa’s volatility, but its meaning. Noise is treated as danger; calm as safety. Yet across Africa, as in all frontier markets, the link between political agitation and investment outcomes is shaped less by the presence of conflict than by the strength of institutions that absorb it.

Drawing on Machiavelli’s argument in Discourses on Livy that political conflict, when institutionalised, strengthens republics rather than weakens them, this framework distinguishes between volatility that can be priced and risk that cannot. Machiavelli was explicit that social and political tension is not a pathology of free systems, but a source of their resilience, provided it is channelled through laws and institutions rather than suppressed by force.

As he writes:

“Those who condemn the quarrels between the nobles and the plebs seem to me to censure the very things that were the first cause of Rome’s keeping itself free.”

And later:

“For in every republic there are two diverse humors, that of the people and that of the great, and all the laws made in favor of liberty arise from their disunion.”

— Niccolò Machiavelli, Discourses on Livy, Book I, Chapter 4.

For investors, the translation is precise. Conflict processed through institutions produces volatility that markets can price. Conflict that overwhelms institutions produces tail risk that markets cannot. The distinction Machiavelli drew about political freedom is the same distinction modern finance must draw about capital safety.

Risk, measured properly

A persistent error in African investing is the conflation of geopolitical risk with investment risk. While the two are often bundled together in headlines, they describe fundamentally different dimensions of capital safety.

Geopolitical risk captures exposure to macro-shocks: regime survival, armed conflict, diplomatic realignment, and social unrest. It is typically proxied by high-frequency datasets such as the ACLED Conflict Index, geopolitical risk sentiment indicators, or composite measures like the Fragile States Index (FSI). This is the weather of a nation—loud, episodic and highly visible. Because it dominates news flow, it is often overweighted by global allocators, even when its transmission to commercial outcomes is indirect.

Investment risk, by contrast, is narrower and more operational. It concerns commercial legibility: whether contracts are enforced, policies evolve predictably, capital can exit, and disputes are resolved through rules rather than discretion. These dynamics are better captured by structural governance measures such as the World Bank’s Worldwide Governance Indicators (WGI) or the Ibrahim Index of African Governance, which illuminate the plumbing of the economy rather than its headlines.

The distinction matters because the two risks do not always move together.

Africa offers repeated examples of divergence. Some countries are politically noisy yet commercially legible—where contestation is channelled through courts, regulators, and markets. Others appear tranquil on the surface while quietly accumulating tail risk, as discretion replaces rules and exit optionality erodes.

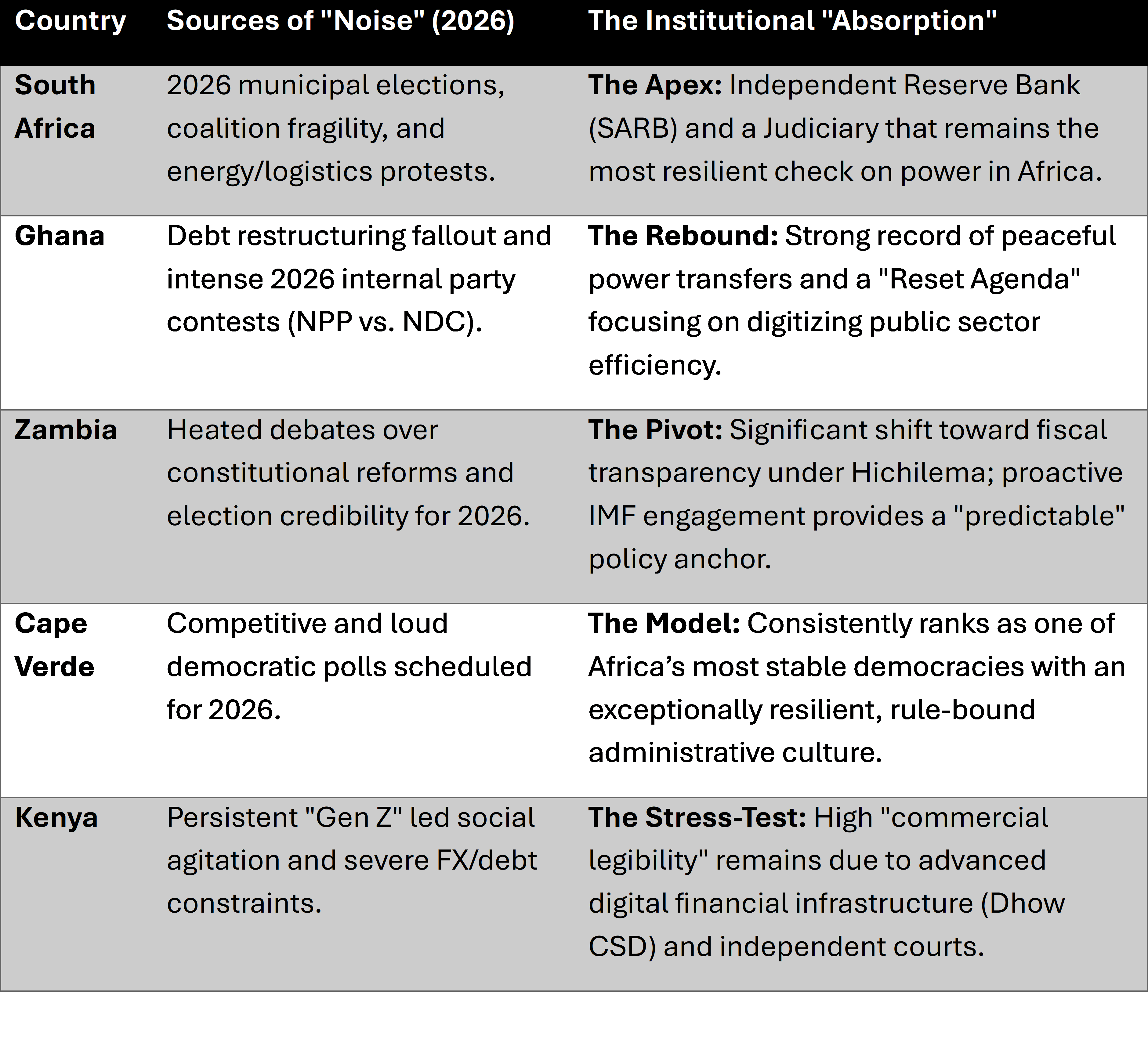

Table 1: Noise is visible. Absorption drives returns. In Africa’s 2026 outlook, institutions, not agitation, separate priceable volatility from unpriceable risk.

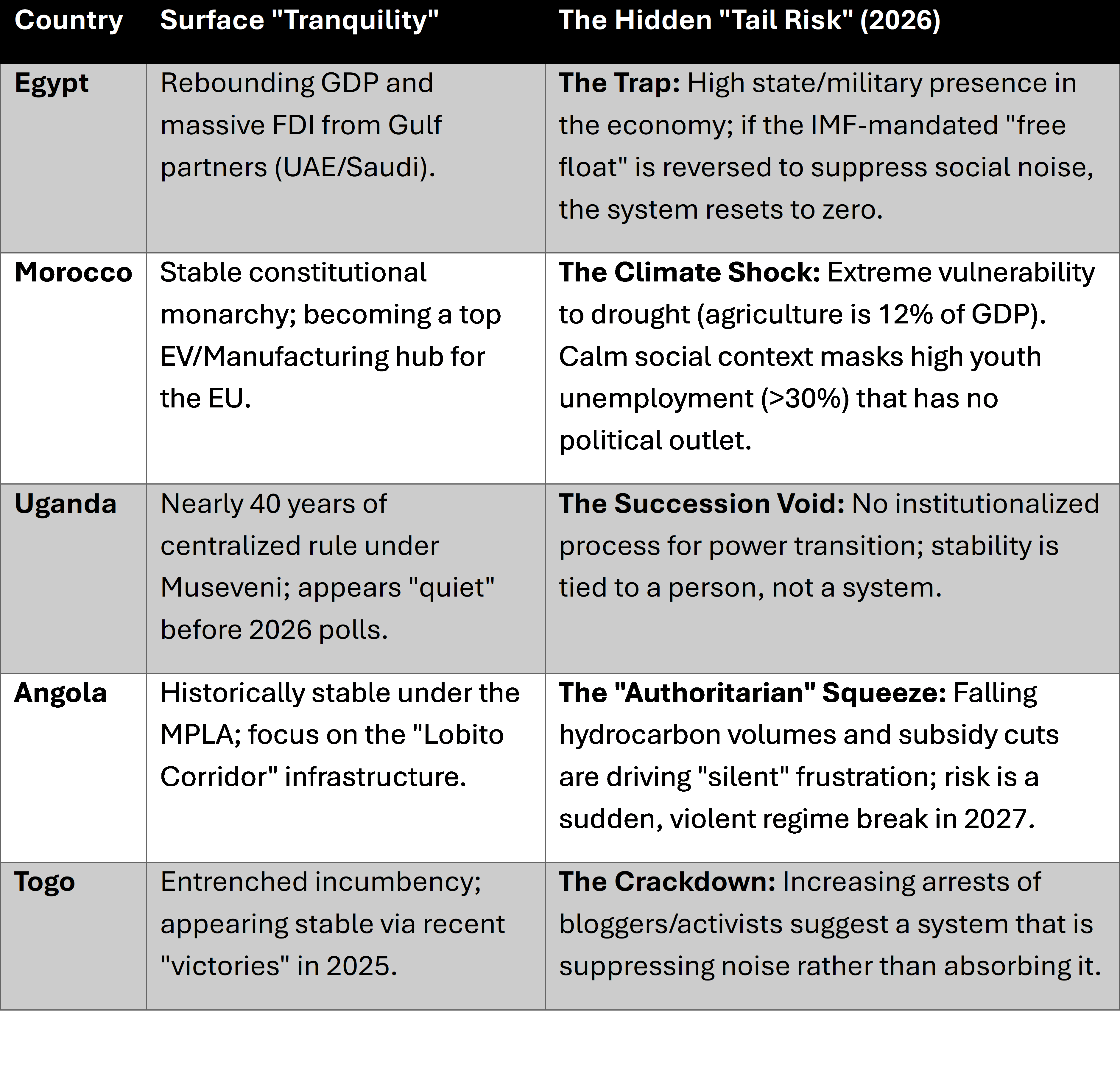

Table 2: Quiet isn’t safe. Institutions are. What looks calm in 2026 can hide tail risk when stability rests on suppression, not systems.

The distinction hinges on a single question: where does pressure go when it emerges?

From philosophy to measurement

To move beyond anecdote, Machiavelli’s observation is translated into a quantitative framework. The analysis maps African countries across two dimensions that determine whether stress becomes a source of renewal or a source of rupture for capital.

Specifically, each country is positioned according to:

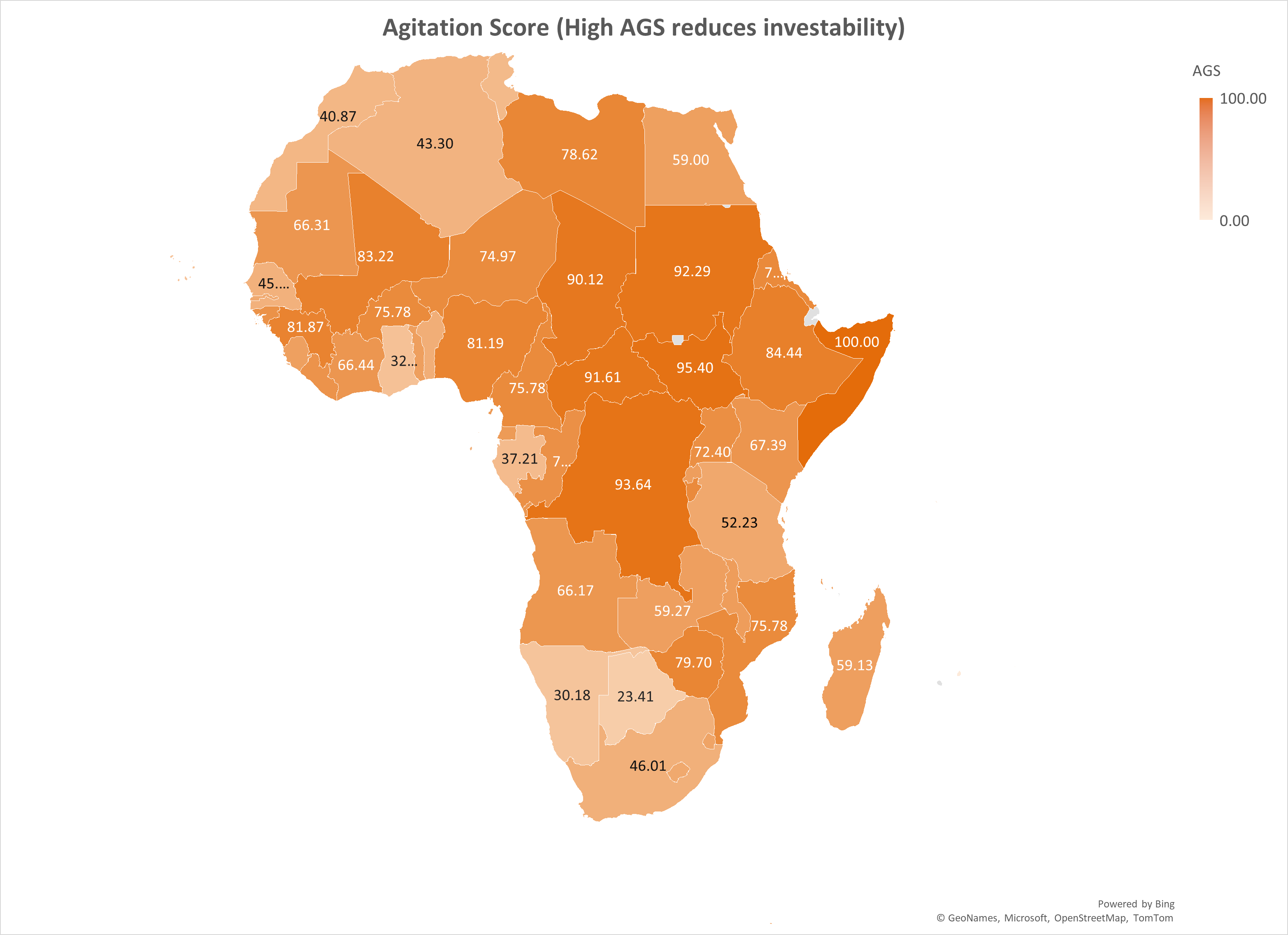

Agitation: is defined as the intensity of political, social, and economic stress that tests a state’s institutional capacity—capturing the frequency and severity of shocks rather than their outcomes. We proxy this dimension using the Fragile States Index (FSI) total score, which reflects pressures across security, legitimacy, and social cohesion. The FSI score is rescaled to a 0–100 Agitation Score (AGS), providing a consistent measure of the stress environment in which institutions must operate and capital must be protected.

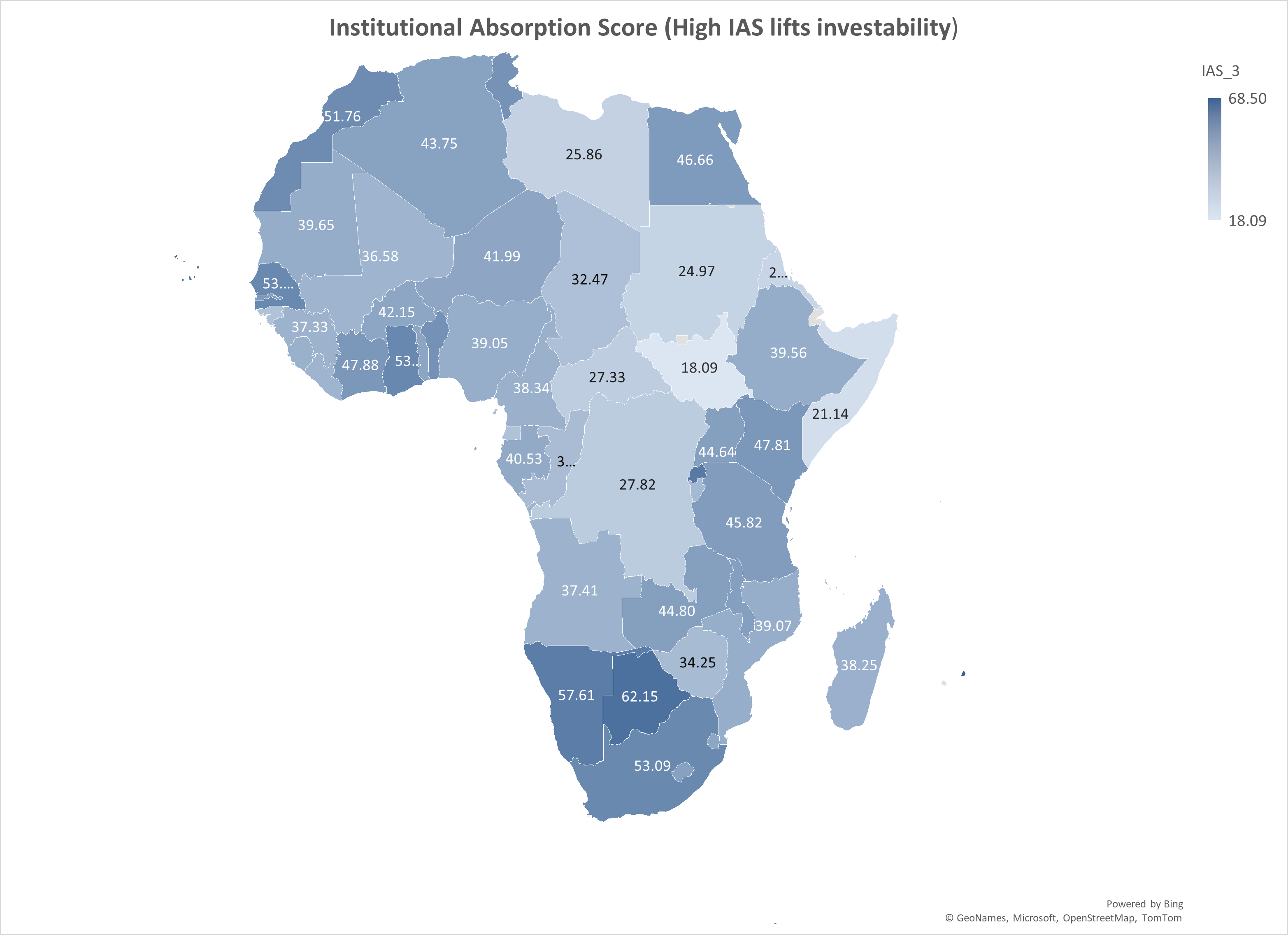

Institutional absorption: defined as the capacity of a state to absorb political and economic stress through rules rather than discretion thus preserving contract enforcement, policy continuity, and credible dispute resolution when pressure rises. We proxy this capacity using the World Bank’s Worldwide Governance Indicators (WGI), combining three dimensions most directly linked to commercial legibility—Rule of Law, Government Effectiveness, and Regulatory Quality. These scores are averaged and rescaled to a 0–100 Institutional Absorption Score (IAS), providing a transparent measure of a country’s ability to protect capital under stress rather than merely in calm conditions.

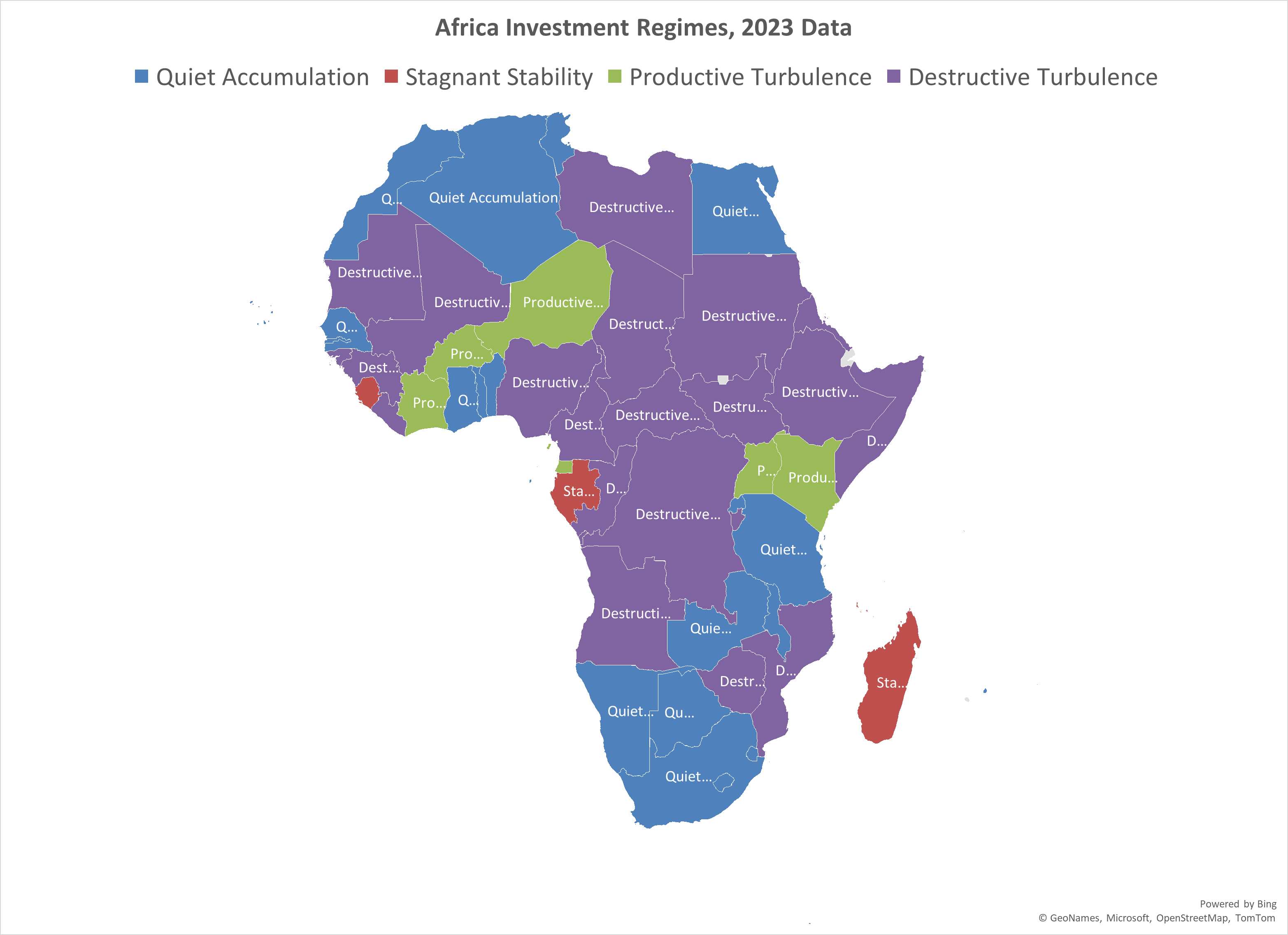

Four African investment regimes

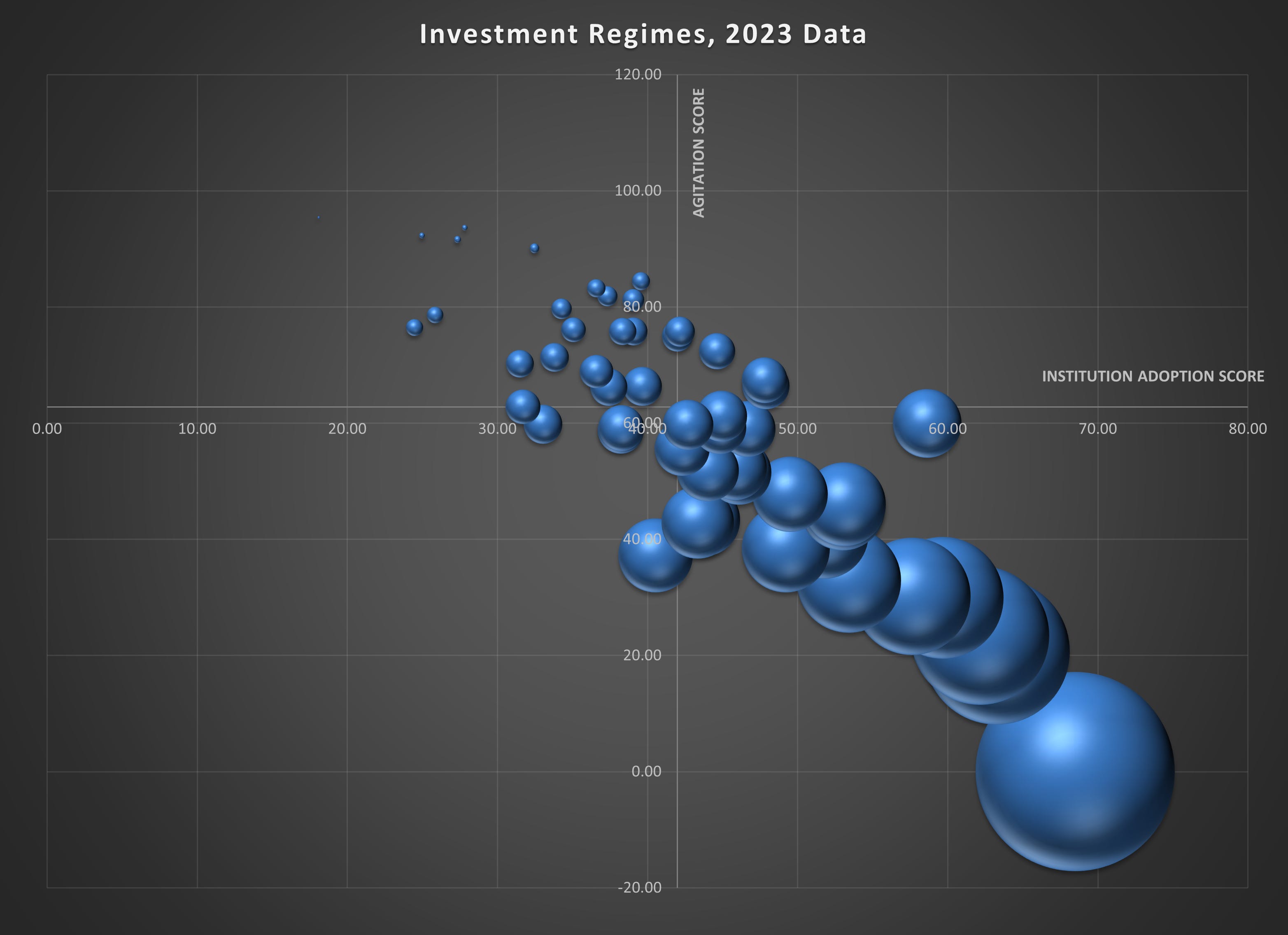

To operationalise the distinction between geopolitical noise and investment resilience, we map African countries on a two-dimensional matrix that combines agitation (measured by the Fragile States Index) with institutional absorption (measured by the Worldwide Governance Indicators). The chart below plots each country against these two forces and draws quadrant lines at the median levels of stress and institutional capacity. The result is not a league table of “safe” and “unsafe” markets, but a regime map revealing four distinct environments in which risk behaves differently and capital requires different instruments. These regimes define the strategic logic for equity, duration, and optionality across Africa.

Plot: Machiavellian Investment Matrix for Africa (Part 1) Scatter plot of all African countries with quadrant lines at median agitation (62.8) and median absorption (42.0).

Map: Machiavellian Investment Matrix for Africa (Part 2)] A plot of African countries with quadrant lines at median agitation and median absorption.

1) Productive turbulence:

High agitation, high institutional absorption.

These are Africa’s most misunderstood markets. Political contestation is visible and frequent, but it is channelled through courts, regulators, elections, and public debate.

Countries in this category, per 2023 data, include Kenya, Ivory Coast and Equatorial Guinea.

For investors, volatility raises pricing error rather than confiscation risk. Capital markets function; exits exist. These environments support public equities, financial infrastructure, scalable platforms, and infrastructure with arbitration frameworks.

Duration tolerance is highest here. Risk is not eliminated but it is compensated.

2) Quiet accumulation

Low agitation, high institutional absorption.

This quadrant is defined by administrative competence and limited contestation. Decision-making is centralised; execution is efficient.

Countries in this category, per 2023 data, include Mauritius, Botswana and Ghana.

These markets favour manufacturing, logistics, export platforms, and policy-aligned real assets. Medium-duration capital performs well. The principal risk is political transition: succession events can reprice assets abruptly precisely because volatility has been suppressed rather than expressed.

3) Stagnant stability

Low agitation, low institutional absorption.

Here, apparent calm conceals weak adaptive capacity. Institutions are slow-moving; discretion substitutes for contestation.

Countries in this category, per 2023 data, include Gabon, Sierra Leone and Madagascar, reward caution. Regulatory drift and informal risk favour short-duration exposure.

Private credit, trade finance, and yield-backed assets dominate. Long-duration equity quietly underperforms, not through crisis but through erosion.

4) Destructive turbulence

High agitation, low institutional absorption.

This is where conflict overwhelms institutions. Rules are suspended rather than tested.

Countries in this category, per 2023 data, include Sudan, South Sudan andSomalia, and parts of the Sahel cluster here.

Investment is possible only through risk transfer: sovereign guarantees, development-finance overlays, or option-like exposure. Balance-sheet capital is structurally misaligned.

Ranking Africa: investability, not optimism

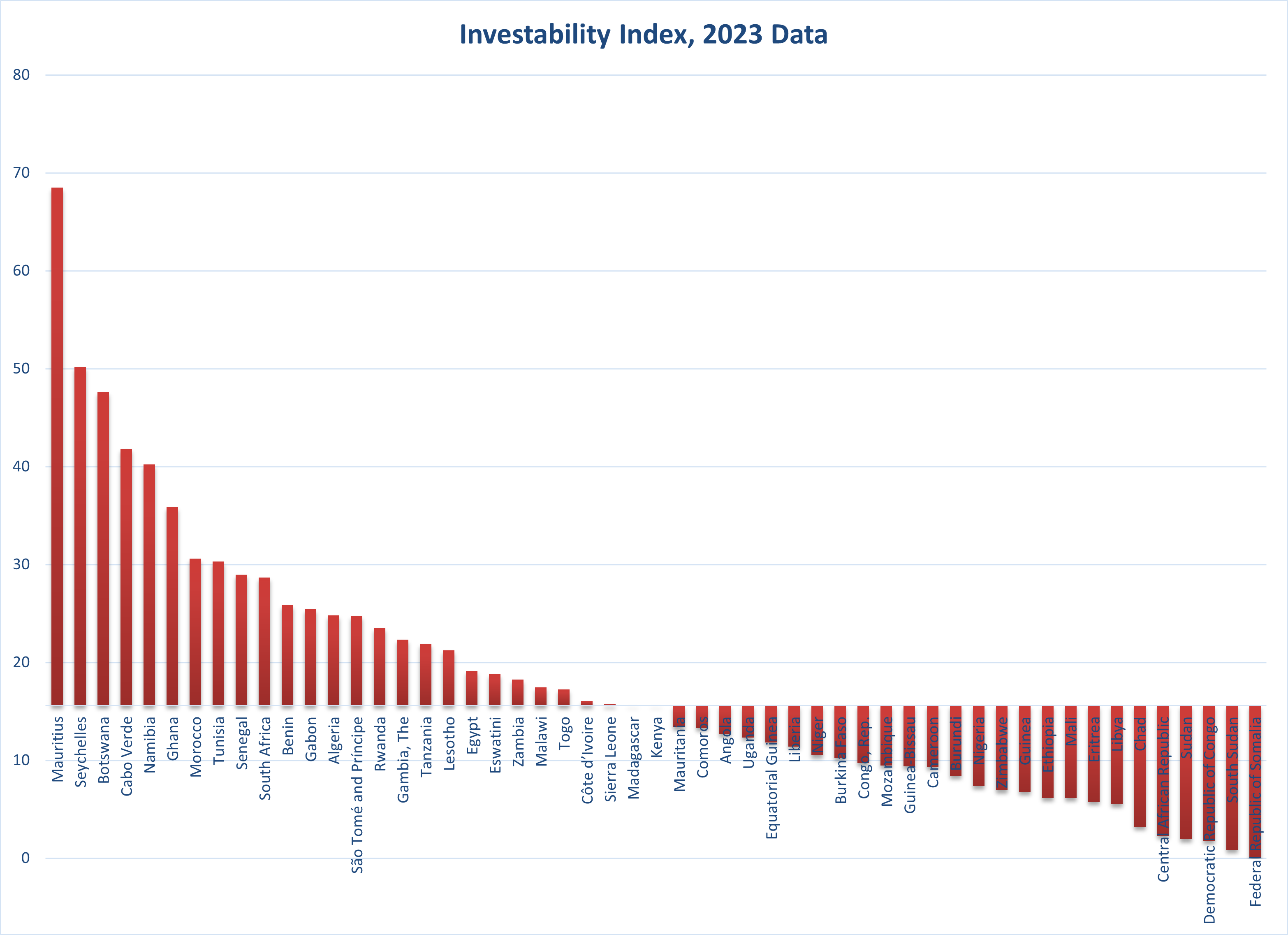

Using the combined FSI–WGI framework, countries can be ranked by a simple but powerful investability score that captures not how often systems are stressed, but how well they absorb that stress when it arrives. The score integrates two forces that investors routinely conflate: agitation, measured by the Fragile States Index, and institutional absorption, measured by the Worldwide Governance Indicators.

In practical terms, this means countries with strong institutions retain high investability even in noisy environments, while those with weak institutions see investability collapse as agitation rises.

By penalising fragility while rewarding rule-based capacity, the resulting ranking distinguishes markets where volatility is merely noisy from those where it becomes destructive to capital. In effect, the investability score does not ask which countries are calmest; it asks which countries remain commercially legible under pressure—and therefore which can sustain equity exposure, duration risk, and long-term capital with confidence.

We scale institutional adoption via and Institution Absorption Score (IAS) into 0–100, then combine it multiplicatively with the agitation penalty via an Agitation Score (AGS):

Investability Index = 100×(IAS/100)×(1−AGS)

Interpretation:

High IAS lifts investability.

High AGS reduces investability.

Countries can remain investable even with agitation if absorption is high.

The Investability Index reveals a distribution across African markets in 2023. The median score of 15.59 forms a natural dividing line between countries where institutions still provide a baseline of capital protection and those where fragility overwhelms absorption capacity. Above the median sit markets where volatility is visible but rules continue to hold; below it lie systems where surface calm can conceal deep structural tail risk. Crucially, the highest-ranked countries are not those with the least noise, but those whose institutions remain strongest relative to the stress they face. This pattern shows that Africa does not face a single “risk problem,” but a deep divide in investability, and it is this divide, not headlines, that should guide long-term capital allocation.

The Africa mispricing

Africa’s capital markets are not uniformly risky. They are unevenly understood.

Global investors too often mistake quiet for safety and noise for danger. Yet history shows the opposite is often true. Systems grow stronger not by suppressing conflict, but by absorbing it through institutions.

For investors, the lesson is direct. Returns accrue where rules hold under pressure: where markets can fail, adjust and recover without breaking.

Across Africa, the most investable markets are rarely the calmest. They are the ones where stress strengthens institutions instead of exposing their absence.

That is why, in Africa more than most places, risk, measured properly, is not a hazard. It is a privilege.

Sources: IMF (2024), Regional Economic Outlook: Sub-Saharan Africa; World Bank (2024), Africa’s Pulse; Fund for Peace (2023), Fragile States Index; World Bank (2023), Worldwide Governance Indicators; African Development Bank (2024), African Economic Outlook; Financial Times and Reuters coverage (2023–2024) on African elections, coups, FX adjustments, and sovereign debt restructurings; Acemoglu & Robinson (2012), Why Nations Fail; North, Wallis & Weingast (2009), Violence and Social Orders.