The 2025 East African Debt Scorecard: Winners, Losers, and Safe Havens

As Kenya cuts rates and Uganda prepares for oil, we compare real returns across 7 nations to find the best entry points for 2026.

Understanding the East African Community (EAC) in late 2025 requires looking beyond individual borders to see the region as a complex, multi-speed credit landscape. The “EAC Story” has fundamentally decoupled: we have moved past a singular focus on “debt distress” into a divergent era of Resource Windfalls vs. Fiscal Consolidation.

While nations like Uganda are successfully de-leveraging through the strategic anticipation of “First Oil” in mid-2026, others, most notably Kenya, are utilizing aggressive fiscal consolidation, anchored by a decisive 4.9%-of-GDP deficit target, to defend their status as regional financial hubs. For the fixed-income investor, the primary challenge is no longer just identifying risk, but accurately timing the monetary divergence between a stabilising Shilling in the East and resource-driven “alpha” in the Albertine Rift.

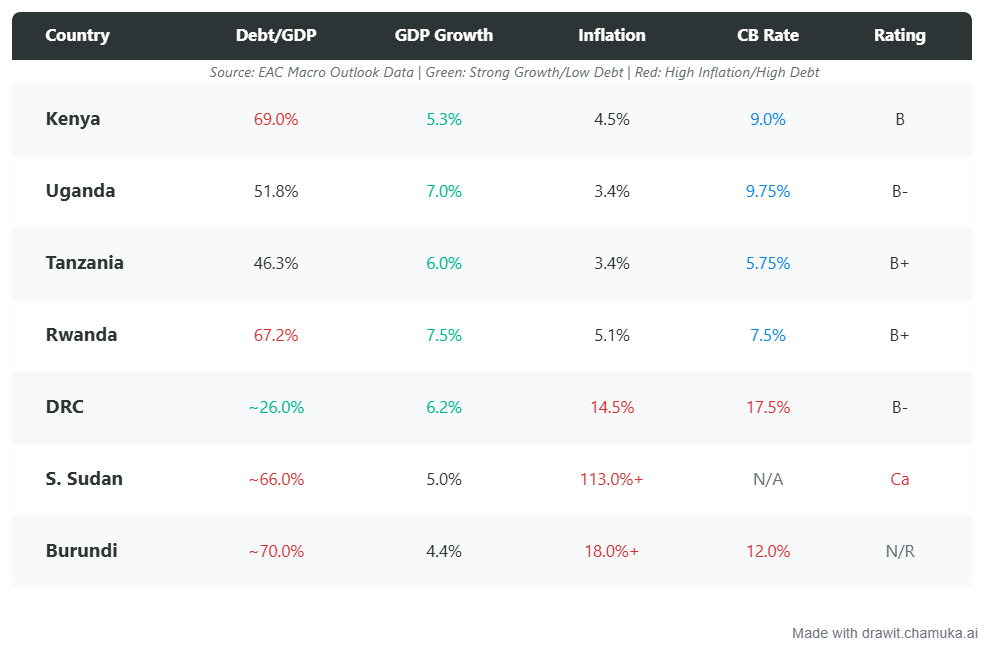

🌏 The 2025 EAC Sovereign Scorecard

Macro-Fiscal Outlook

🔍 Analysis: The Three Tiers of EAC Debt

1. The “Stability & Scale” Tier (Kenya & Tanzania)

Kenya: The regional financial heavyweight. After a volatile 2024, Kenya enters late 2025 with a “consolidation win.” Inflation has cooled to ~4.5%, allowing the Central Bank of Kenya (CBK) to maintain its easing cycle. Debt-to-GDP is stabilizing near 69% as the government prioritizes local currency borrowing to mitigate exchange rate shocks.

Tanzania: Widely considered the most stable “safe haven” in the region. With the lowest debt-to-GDP among major EAC economies (~46%) and massive investments in the Standard Gauge Railway (SGR) and hydropower, Tanzania is leveraging its fiscal space to become the region’s logistics heart.

2. The “Resource & Growth” Tier (Uganda & Rwanda)

Uganda: 2025 is the “Eve of Oil.” Markets are pricing in a massive revenue jump for 2026 as crude output nears. While domestic debt grew in 2024, the outlook is bolstered by expected USD inflows from the EACOP pipeline. S&P recently upgraded Uganda’s outlook to Positive.

Rwanda: Despite a high debt ratio (67%), Rwanda remains a darling for concessional lenders. Its growth (7.5%) is the fastest in the region, driven by the service sector and professionalized agriculture. Its debt is “expensive” in volume but “cheap” in interest due to the high share of multilateral loans.

3. The “Frontier & Fragile” Tier (DRC, Burundi, South Sudan)

DRC: An anomaly with low debt but high risk. The 26% debt-to-GDP reflects limited market access rather than fiscal discipline. Investors here focus on mining-backed credit and private equity rather than sovereign bonds.

Burundi & South Sudan: Both face severe FX shortages and hyper-inflationary pressures. They remain heavily reliant on commodity prices and, in Burundi’s case, slow donor re-engagement.

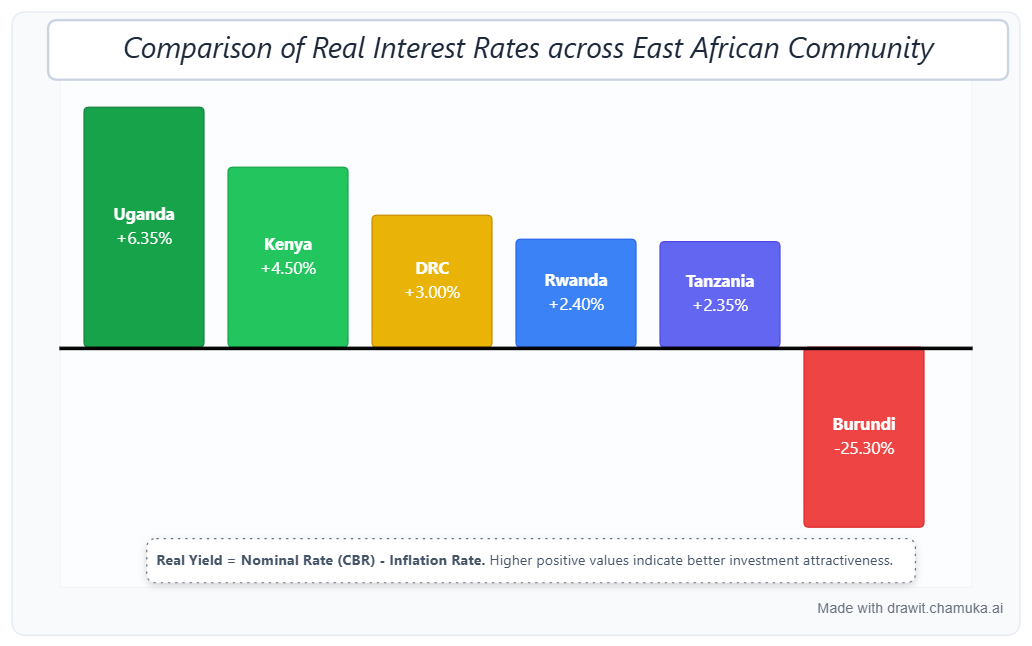

📈 The Real Yield Heatmap

For fixed-income investors, the critical metric isn’t the coupon rate, but the Real Yield, the return you keep after accounting for inflation. In 2025, the region offers some of the most compelling real yields in the frontier market space.

Uganda: The “Yield Darling” of the EAC

While Kenya often dominates regional headlines, Uganda is currently delivering the East African Community’s most compelling risk-adjusted real return. As of late 2025, the investment case has shifted from a high-yield carry trade to a structural de-leveraging play ahead of “First Oil” in mid-2026. With inflation anchored at 3.4% and the policy rate held at 9.75%, investors are netting a remarkable +6.35% real yield, supported by foreign exchange reserves that hit an all-time high of USD 5.4 billion in late 2025. To curb the debt-service burden, which now consumes nearly a third of domestic revenue, the Ministry of Finance has announced a decisive 21.1% cut in domestic debt issuance for the FY2026/27 cycle. This supply-side squeeze, combined with S&P’s recent shift to a Positive Outlook, positions Ugandan local bonds as a premier “alpha” opportunity for investors looking to front-run a projected 10.4% GDP surge in 2027.

Kenya: The “Soft Landing” Hub

Kenya enters 2026 as the EAC’s leader in monetary consistency, having transitioned from the “maturity cliff” fears of 2024 to a sustained period of growth support. By delivering its ninth consecutive rate cut in December 2025, bringing the policy rate down to 9.0%, the Central Bank of Kenya (CBK) has successfully anchored inflation at 4.5% and stabilized the Shilling below the 130.00 mark. While public debt remains elevated at ~68.8% of GDP, record foreign exchange reserves of $12.1 billion and a successful pivot toward domestic “Switch Auctions” have significantly lowered refinancing risks. For investors, Kenya represents a +4.50% Real Yield and a prime duration play, offering deep liquidity and the potential for significant capital gains as benchmark bond yields continue their downward “bull flattening” trajectory.

DRC: The Resource-Rich Paradox

The Democratic Republic of the Congo (DRC) is the EAC’s most distinct credit profile, an “under-leveraged” economy where a low debt-to-GDP ratio of ~26.0% masks high structural fragility. Entering 2026, the DRC is a play on aggressive disinflation. Under strict IMF-backed discipline, the Central Bank has crashed inflation from over 20% to just 2.2% as of late 2025. While this creates a staggering theoretical spread against the 17.5% policy rate, the “Real Yield” for investors is a more modest +3.0% once adjusted for chronic currency volatility and the lack of secondary market liquidity. While copper and cobalt exports provide a robust fiscal anchor, investors must navigate persistent security overruns in the East and a “predatory” tax system that keeps the DRC a Tier-3 sovereign destination for all but the most risk-hardened capital.

Rwanda: The High-Growth Leveraged Play

Rwanda remains the EAC’s growth champion, with GDP expanding by a staggering 11.8% in Q3 2025, yet this momentum is tightly coupled with rising leverage. While the public debt-to-GDP ratio has climbed toward 73.2% (projected to peak near 80% by 2027), the risk of distress remains “Moderate” because two-thirds of its debt is concessional. This favorable structure shields Rwanda from the high interest burdens seen in Kenya, allowing it to fund “Mega-Projects” like the New Kigali International Airport and RwandAir expansion. For investors, Rwanda offers a balanced +2.40% Real Yield; it is a “Strategic Hold” that prizes world-class governance and infrastructure-led growth over the high-octane carry trades of its neighbors.

Tanzania: The Safe Haven Under Pressure

Tanzania enters 2026 as the EAC’s leading macroeconomic anchor, maintaining a debt-to-GDP ratio of 46.3%, the only major regional economy under the 50% threshold. However, its “Safe Haven” status is transitioning from a passive guarantee to a strategic watch. Following the contested October 2025 elections, the “Legitimacy Discount” has arrived: Western donors, led by the European Union, have begun suspending aid packages (projected 20% ODA contraction), forcing a costly pivot toward non-concessional commercial debt and domestic borrowing. While the +2.35% Real Yield remains a stable “cash proxy,” investors must now weigh the country’s robust infrastructure-led growth against rising political risk and the potential for a 1–2% drag on GDP if diplomatic isolation persists.

Burundi and South Sudan: The Fragile Frontier

Burundi and South Sudan currently represent the most distressed credit profiles in the EAC, where hyperinflation and severe currency instability have rendered traditional “Real Yield” metrics a measure of capital destruction. Burundi is trapped in a negative real-interest spiral (approx. -25.30%), exacerbated by the January 2025 termination of its IMF program and a chronic FX shortage that limits import cover to just 1.6 months. Meanwhile, South Sudan is navigating an existential fiscal crisis following a massive 30% GDP contraction in FY25 due to oil pipeline shutdowns in Sudan. While oil exports resumed in late 2025, the economy remains crippled by triple-digit inflation and a USD 2.3 billion oil-backed debt wall. For investors, these markets remain “observational” only; until exchange rates are unified and commercial arrears cleared, they serve primarily as a cautionary backdrop to the more liquid hubs of Kenya and Uganda.

⚠️ Regional Risk Watch: 2026 Outlook

Monetary Divergence: While Kenya and Tanzania ease, the DRC and South Sudan remain in high-interest environments to combat structural inflation.

Refinancing “The Wall”: Kenya and Rwanda face significant commercial debt maturities in 2026. Their ability to tap international markets at sub-10% coupons will be the litmus test for regional sentiment.

Currency Stability: The Kenyan Shilling has remained steady at the 128-130 range, acting as a “stability anchor” for regional trade.

The Impala Market Strategy for 2026

For fixed-income investors, the EAC in 2026 is defined by a “monetary decoupling.” impacted by key fiscal calendar events.